Changing South-South trade and investment dynamics

All the versions of this article: [English] [Español] [français]

Changing South-South trade and investment dynamics

bilaterals.org and GRAIN

September 2007

Most people think of international trade politics in terms of typical North-South dynamics: the rich imperialist North bullies the poor and downtrodden South. Yet, while North-South FTAs and investment treaties continue to be the most potent vehicles to make the world a better place for the North’s TNCs, South-South FTAs and the rise of Southern TNCs constitute important new realities forcing us to change the way we look at global economic and power relations, especially when viewed from the South.

The new South-South axis

Globally, South-South trade represents only about 6% of all trade in goods and 10% of all trade in services. But it is growing relatively fast, at 11% per year, from a low starting point not long ago. [1] Of Africa’s exports, 27% now go to Asia, almost on a par with its exports to the EU (32%) or the US (29%). [2] Half of all trade of Asia’s developing countries is conducted between themselves. [3] So we cannot look at everything through a North-South prism.

South-South investment, on the other hand, is where things are really jumping. [4] Hardly a day goes by without the local papers in Mumbai or São Paulo reporting on new investment deals being struck by developing country TNCs, or governments on their behalf, in other developing countries. Often these are big infrastructure, extraction, manufacturing or processing projects: Argentina’s soybean king developing plantations in Venezuela, China signing a mega-loan with the Democratic Republic of Congo to be paid back in cobalt, the Malaysians clearing fields for palm oil production in Mindanao (Philippines), Zambia’s state-run Electric Supply Corporation signing a US$150m deal with India’s Tata empire to build a new power plant, and so on. Sometimes these ventures concentrate purely on restructuring finance, like the creation of the all-new Bank of the South in Latin America or China’s recent cancellation of US$1.3 billion in African debt. But finance aside, the production-oriented South-South business deals are multiplying for simple reasons: they provide easier access to credit; the technology is not so complicated to transfer; the companies understand the working conditions in other developing countries; and they provide at least some veneer of domestic sovereignty or control. Most of all, there is clearly a strong political motivation on the side of the national elites to make such ventures work.

With more and more money concentrated in the hands of Southern capitalists — whether private consortia, family dynasties or state-owned firms — this overall momentum towards increased South-South wheeling and dealing is starting to change the shape of the world economy.

The rise of southern TNCs (and not a few state capitalists)

Drawing from UNCTAD’s latest statistics (2006): [5]

- A quarter of all TNCs in the world are from developing and transition countries. In 1990, 19 appeared in the Fortune 500 list of the world’s most important corporations. In 2006, there were 57 on the list.

- Leaving out the transition economies like Russia and Turkey, developing countries with the most homegrown TNCs today are Mexico, Brazil, South Africa, China, India, Thailand and Malaysia. In fact, Mexico is home to the third richest person in the world, Carlos Slim Helu, who has made a fortune buying up telecommunication companies in Latin America.

- Eighty of the top 100 TNCs from developing countries today are Asian. Many of them have their roots in the Chinese diaspora.

Most operations of these new Southern corporations are conducted within their respective regions. Chilean TNCs mostly invest in Latin America while Thai TNCs try to build their own fiefdoms in neighbouring Asian countries. In some cases, this is stoking perceptions of regional hegemons, particularly as the biggest powerhouse economies like India, China, Brazil and South Africa make substantial inroads into nearby countries, setting up businesses, getting access to land and taking an increasing share in sensitive local industries like infrastructure development. Tensions develop when issues of sovereignty over natural resources, pollution, labour complaints and political string-pulling emerge from these deals. The recent public outcry in the Philippines over various Philippine-China agreements, from telecommunications to farming, is a good example of this.

So how many South-South corporate deals are inked each year? It’s hard to say. [6] Worldwide, the number of cross-border mergers and acquisitions concluded doubled between 1990 and 2004. (There were roughly 2,500 deals signed in 1990 and 5,000 in 2004.) The share of developing countries in this investment spree went up sixfold. (On the buying side, they represented 5% of all foreign business acquisitions in 1990 and 16% in 2004. On the selling side, they accounted for 7% of all cross-border deals in 1990 and 20% by 2004.) The problem is that this data doesn’t speak for Southern-owned capital alone. A lot of these deals are conducted by local affiliates of Northern transnationals. The data also doesn’t distinguish between public and private operations. A lot of major transnational corporations in the South are still, despite privatisation drives, state-owned.

All told, according to the OECD, the biggest investor in South-South mergers and acquisitions is Singapore, followed by China, Malaysia and South Africa. [7]

The China factor...

China alone stands out very visibly in today’s boom in South-South trade and investment deals. It is now the second largest investor in Africa, just behind the USA, and is building a larger presence for herself in many countries of Asia and Latin America. This is not just about flooding markets with plastic toys or flimsy T-shirts, at prices many countries cannot compete against because of low labour costs. The big push behind China’s outward expansion is its huge need to import energy and other so-called raw materials to fuel its economic growth. China’s thirst for oil and gas, followed by minerals, is the main reason why it is investing so much in Africa right now — and pouring vast sums of money to build the infrastructure to physically move the stuff, especially across neighbouring countries in Central and Southeast Asia. [8] China is also investing heavily in growing food crops in neighbouring countries as a source of agrofuel for its own energy production. The Chinese have signed deals to produce sugar cane and cassava for this purpose in Indonesia [9], hybrid rice, cassava, maize and sugar cane in the Philippines, [10] and are starting to explore opportunities to develop agricultural production - along with five export processing zones - in Africa. [11] The signing of the China-Thailand FTA brought a huge leap of Chinese investment in northern Thailand, with 100 Chinese firms now operating there, [12] engaging US$277 million in capital in this otherwise quiet region. [13] Chinese banks, especially the China Development Bank (CDB) and other Chinese players, have also invested in a number of foreign banks and financial companies. Many Chinese TNCs emerged from state companies and/or expanded through the acquisition of state companies.

China, which has long been the number one destination for foreign investment going to the South, is now becoming a major foreign investor, especially in other developing countries. This is due not only to the dramatic growth of capital accumulation in China but to equally dramatic shifts in state policy, with the Communist Party announcing in 2002 its "Go Out" programme to rely no longer on export-led growth, and to promote Chinese foreign investment. [14] It is very hard to get reliable and uncontradictory figures, but according to the Ministry of Commerce in Beijing, Chinese companies invested US$21 billion abroad in 2006 alone, of which US$17 billion was in the non-financial sector. [15] This adds up to 5,000 Chinese companies running 10,000 business operations in 172 countries, with an accumulated outward investment stock of some US$50-70 billion.

As to the future, a 2006 survey conductedfor the World Bank [16] shows that 60% of consulted Chinese companies planned to make new investments abroad in the years ahead, with South Asia, East Asia and Africa topping the list of preferred destinations. Their main motivations? Access to markets, access to "strategic assets" and global competitive strategies.

... but also the Gulf and others

The Gulf Arab states, which have their own regional integration project through the Gulf Cooperation Council (GCC) and strong commitments to the development of both the Arab League and the Organisation of the Islamic Conference, are another central spot in the fast strengthening South-South trade and investment map. For one, everyone these days seems to want to do business with, or in, the GCC member states. [17] For many, there is huge money to be made in the Gulf, especially if you can get privileged investment access under an FTA. The queue for GCC FTAs is growing daily. But the Gulf States are also becoming expansive outward investors — mostly buying bits and pieces of major operators in developed country markets but also injecting money into developing countries. In 2006, the Gulf states invested US$30.8 billion abroad. As for 2007, by September they had already doubled the 2006 figure and spent US$64 billion in foreign investment. [18] The top outward Gulf investors in dollar terms are the UAE, Kuwait, Saudi Arabia and Bahrain.

Some snapshots give an idea of what’s going on:

- Dubai’s top property developers — Emaar, Dubai Holding and Dubai World, all predominantly owned by the Maktoum family — are building on a massive scale for high-end markets in Syria, Pakistan, Jordan, Egypt, Lebanon, Libya, Morocco and half a dozen other developing countries around the world. [19]

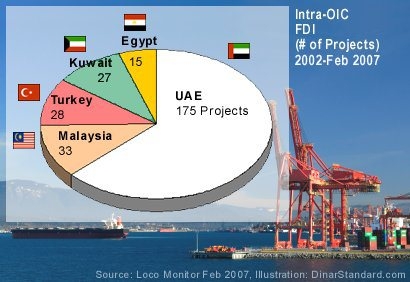

- Cross-border investment between countries of the OIC is growing. The United Arab Emirates are by far the biggest investor in fellow OIC states (see Figure 1), while the top recipients of intra-OIC investment are Saudi Arabia, Jordan, Syria, Indonesia and Lebanon, each getting about 25 projects from other OIC states between 2002 and 2007. [20] The OIC is important because it is a community of mostly developing countries united around a common political agenda, with a strong capacity for solidarity.

- As Gulf states try to capitalise on record oil prices and at the same time address the need to diversify away from oil revenues, there is a great amount of cross-border investment going on in sectors like banking and telecommunications, both among themselves and reaching out to Middle East neighbours such as Egypt and Syria.

But there’s plenty more. According to a March 2007 study by the Associated Chambers of Commerce and Industry of India (ASSOCHAM), India’s investment outflows were expected to hit US$15 billion in (calendar) 2007, outstripping investment flows going into India. [21] The Federation of Indian Chambers of Commerce and Industry (FICCI) and Ernst & Young put out another report in June 2007 claiming the figure will hit US$35 billion for fiscal 2007-8. [22]

Most of India’s outward investment — concentrated in the IT, automobile and pharmaceuticals sectors — goes to the USA or Europe. But Africa comes in third place and the pace of change is fast. While sub-prime loans may rock the USA, there is clearly no credit crunch in India!

In Latin America, outgoing investment from TNCs and state enterprises in the region jumped by 115% to US$41 billion in 2006. Most of this is attributed to the rapid internationalisation of a few major corporations in Brazil and Mexico [23] — much of it being pumped into neighbouring Latin American and Caribbean states.

The table below summarises the top echelon of South-South investment activity over the past 17 years, by source country.

Table: Most active South-South corporate investors, in mergers & acquisitions only, by home country (1990-May 2007)

| Home country | Value of deals (US$ billions)) |

|---|---|

| Singapore | 35.8 |

| China | 18.3 |

| Malaysia | 12.7 |

| South Africa | 11.6 |

| United Arab Emirates | 7.2 |

| Brazil | 6.7 |

| Chile | 6.1 |

| India | 4.7 |

| Qatar | 4.7 |

New partners or new rivals?

With more and more money flowing between developing countries, two things are bound to happen. First, the role of Northern capital — whether it comes from the IMF or development cooperation agencies like USAID or ministries of foreign affairs — is bound to shrink a bit. In many cases, this is deliberate. The Bank of the South in Latin America is meant to replace both the InterAmerican Development Bank and the IMF in providing loans and other forms of working capital in the region. And China has a strong political agenda to provide not only investment but soft credit arrangements with very different strings attached than those coming from Northern sources, to build its political alliance base. [24] For the most part, this is a good thing. But it would be foolish to think that because it is South-South it is inherently better. How much developing country governments push and further entrench neoliberalism in their cross-border trade and investment dealings is the key issue. Chávez aside (and maybe not!), they might turn out as bad any Northern government.

Secondly, rivalries and resentments are sure to emerge. This is already clear in Latin America, where ideological differences and competing business interests are behind various tensions in cross-border trade and investment endeavours (see Raúl Zibechi, "Integration or free trade?"). In Asia, India and China have significant competing and conflicting interests, even though this is often played down in diplomatic spheres. Both Pakistan and Bangladesh are important theatres of this rivalry, and as Chinese investments in these countries grow, the political tension with Delhi may also increase. In Africa, there are many social, and even governmental, problems with China’s growing economic role in the region, particularly since China tends to bring its own labour force to implement its funded projects. While China is trying to address this, its strategic emphasis on setting up export processing zones — which come with their own intrinsic set of problems — may outweigh some of the palliative efforts to cut back on the importation of a Chinese workforce.

The shape of global economic forces is changing rapidly today, with South-South trade and investment starting to grow rapidly just as developing country governments turn to bilateral FTAs and regional economic integration efforts with more zeal. Where this will take us remains to be seen. For certain, though, the growth in wealth and power of Southern TNCs and the aggressive teaming up of developing country governments to reshape finance and investment flows between them will change domestic Southern economies in the years ahead. Further examination is warranted of the dynamics of Southern stock market flows, the implications of Southern companies selling public shares, and the levels of integration with Northern capital. How much all of this serves to deepen class divisions, to further the dismantling of redistributive models and promote neoliberal paradigms of unbridled privatisation is the real question.

Footnotes:

[1] Organisation for Economic Cooperation and Development, "South-South trade: vital for development", OECD, Paris, 2006. https://www.oecd.org/dataoecd/30/50/37400725.pdf

[2] Harry G. Broadman, "Africa’s Silk Road: China and India’s New Economic Frontier", World Bank, Washington DC, 2007. As Broadman points out, the EU’s share of Africa’s exports has actually been sliced in half in recent years. http://go.worldbank.org/PKNA9OP5E0

[3] United Nations Conference on Trade and Development, Trade and Development Report 2007, UNCTAD, Geneva, 2007. http://www.unctad.org/Templates/WebFlyer.asp?intItemID=4330&lang=1. The figure is 20% for Latin America and 10% for Africa.

[4] See United Nations Conference on Trade and Development, World Investment Report 2006, UNCTAD, Geneva, 2006, http://www.unctad.org/en/docs//wir2006_en.pdf

[5] United Nations Conference on Trade and Development, World Investment Report 2006, UNCTAD, Geneva, 2006. http://www.unctad.org/en/docs//wir2006_en.pdf

[6] The following data come from UNCTAD’s "Beyond 20/20" WDS database: http://stats.unctad.org/FDI/

[7] Hans Christiansen et al., "Trends and recent developments in foreign direct investment", OECD, Paris, June 2007, p. 15. http://www.oecd.org/dataoecd/62/43/38818788.pdf

[8] See, for example, Marwaan Macan-Markar, "China turns Mekong into oil-shipping route", IPS, Bangkok, 5 January 2007, http://ipsnews.net/news.asp?idnews=36074 and Raphael Minder and Isabel Gorst, "Historic Asia trade route to be rebuilt", Financial Times, London, 18 September 2007, http://www.ft.com/cms/s/0/8c7b80e8-6604-11dc-9fbb-0000779fd2ac.html

[9] "China’s Bright Food ties with Salim to grow abroad", Reuters, 18 January 2008., http://www.flexnews.com/pages/10258/China/Dairy/chinas_bright_food_ties_salim_grow_abroad.html

[10] GRAIN, "Hybrid rice and China’s expanding empire", 6 February 2007, http://www.grain.org/hybridrice/?lid=176.

[11] Cole Mallard, "China continues gaining economic equity in Africa through agricultural investment", Voice of America, Washington DC, 23 August 2007, http://www.voanews.com/english/Africa/2007-08-23-voa26.cfm

[12] Stephen Frost, "Chinese outward direct investment in Southeast Asia: How much and what are the regional implications?", Southeast Asia Research Centre, City University of Hong Kong, Working Papers Series No. 67, July 2004, http://www.cityu.edu.hk/searc/WP67_04_Frost.pdf

[13] Thai Board of Investments, quoted by Lorine Schaefer, "Outward direct investment: China in Africa, Southeast Asia, and Brazil", Global Interdependence Center, http://www.interdependence.org/Outward%20Direct%20Investment-China%20in%20Africa,%20Southeast%20Asia,%20and%20Brazil.doc

[14] Yuen Pau Woo and Kenny Zhang, "China goes global: the implications of outward direct investment", Asia Pacific Foundation of Canada, 2006, http://economics.ca/2006/papers/0892.pdf. According to the US consultancy group Accenture, part of Beijing’s "Go Out" policy is to nurture 10-20 "national champions" — key state-owned firms that will be propped and padded — in China’s outward economic drive. See "China spreads its wings", Accenture, 2005 at http://www.accenture.com/NR/rdonlyres/6A4C9C07-8C84-4287-9417-203DF3E6A3D1/0/Chinaspreadsitswings.pdf

[15] "China invests billions abroad", Manufacturing.net, 17 September 2007, http://www.manufacturing.net/China-Invests-Billions-Abroad.aspx

[16] Joe Battat, "China’s outward investment", 13 April 2006, at http://psdblog.worldbank.org/psdblog/2006/04/chinas_outward_.html

[17] Halliburton, the Houston-based US defence contractor, opened a second headquarters in March 2007 in Dubai.

[18] Andrew Ross Sorkin, "The Mideast money flows", New York Times, 27 September 2007.

[19] Emily Flynn Vencat, "Dubai’s glitz goes global", Newsweek, 30 October 2006 at http://www.msnbc.msn.com/id/15359298/site/newsweek

[20] Sajjad Chowdhry, "Foreign direct investment (FDI) on the rise in OIC economies", DinarStandard, 10 April 2007 at http://www.dinarstandard.com/current/OIC_FDI040907.htm

[21] "FDI outflow of $15 billion likely in 2007", News behind the news, 19 March 2007. http://www.news.indiamart.com/news-analysis/fdi-outflow-of-15-bi-15100.html

[22] "FDI outflow may touch $35 bn: study", Financial Express, 18 June 2007, http://www.ficci.com/news/viewnews1.asp?news_id=1195.

[23] "Latam and Caribbean show huge FDI outflow increase", Foreign Direct Investment Magazine, 6 August 2007. http://www.fdimagazine.com/news/fullstory.php/aid/2067/Latam_and_Caribbean_show_huge_FDI_outflow_increase.html

[24] For instance, adherence to the "one China" policy — including no formal relations with Taiwan — is expected of countries on the receiving end of Beijing’s neoliberal largesse. Given the history of the Cold War period, China’s network of investment and loan recipients may also be expected to support the PRC in its political leanings at the UN Security Council. Further, China’s investments in Africa have generated a wave of Presidential Investment Advisory Councils which are high-level national fora through which Beijing can interact directly with local captains of industry, whether domestic or TNC affiliates, to discuss and potentially advise changes in the local business environment, including national policies. (See Broadman, Africa’s Silk Road, World Bank, Washington DC, 2007, pp 146-147.)